Know Before You Build: Considerations for Building in a Flood Zone

Understanding the Risks

In South Louisiana, it's common for homes—even new builds—to be located in flood zones. That doesn’t mean you shouldn’t build there. But it does mean you need to plan differently.

Flood zones are classified by FEMA based on the likelihood of flooding. If your property falls into a Special Flood Hazard Area (SFHA)—such as Zone AE or VE—there are added requirements for how your home must be constructed and insured.

These rules affect not just where you build, but how high you build, what kind of insurance you’ll need, and how long permitting may take.

“The time to address flood risk is during the planning stage—not after breaking ground.”

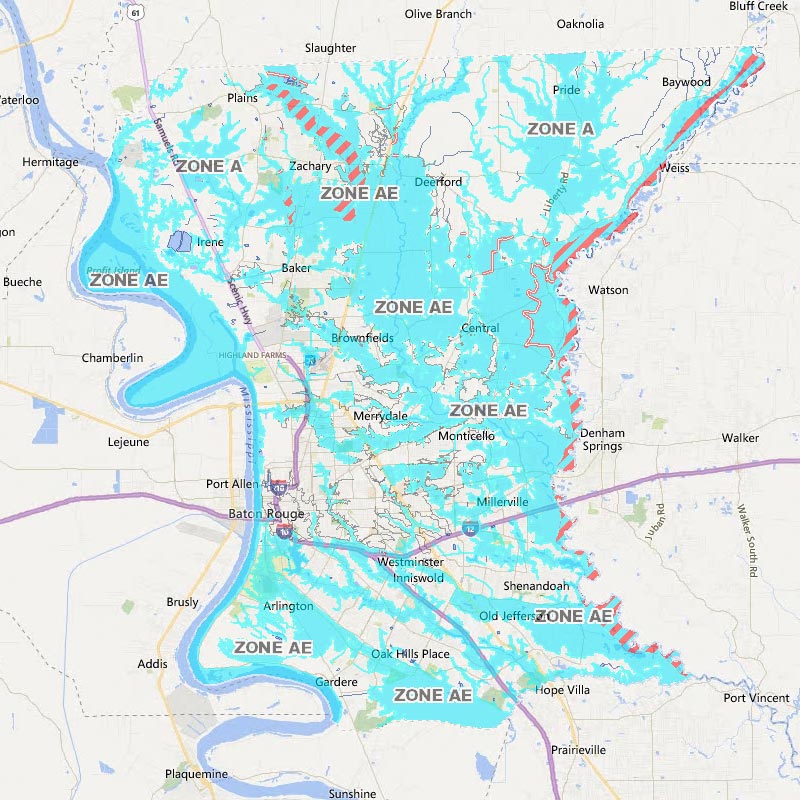

How to Check a Property’s Flood Zone

To find out if a property is in a flood zone, start by searching your location using these tools:

These tools help identify whether the parcel is in a hazard zone. However, they do not replace the accuracy of a professional survey. For that, we always recommend ordering a proposed elevation survey before purchase.

This survey should include a FEMA-compliant elevation certificate, and many local surveyors will mark a nearby object like a nail or pole with the elevation reference. You can also request a Flood Hazard Determination Review from FEMA.

Construction Impacts and Elevation Options

If your lot falls below the Base Flood Elevation (BFE), you may need to build up the ground or elevate the foundation with a pier or stemwall system. In some cases, fill dirt can be used, but this typically triggers the need for a Letter of Map Revision based on Fill (LOMR-F).

In other situations—especially if the natural ground is already above the BFE—you may qualify for a Letter of Map Amendment (LOMA) that can remove the flood insurance requirement altogether.

But even when you're technically above the BFE, you may still need to elevate higher. Many local parishes and municipalities require building several feet above FEMA's minimums in exchange for better community-wide flood insurance ratings. These extra height requirements, known as freeboard, are designed to improve safety and reduce insurance premiums over time.

Important: FEMA flood maps are updated every few years. After the 2016 flooding in Greater Baton Rouge, many areas were reclassified, and BFE data was delayed or revised. A map check from years ago is no longer valid today.

We strongly recommend that buyers do not rely solely on a seller’s or agent’s word—only an up-to-date survey and FEMA maps can confirm your status.

Flood Insurance and Lender Requirements

If your land is in a Special Flood Hazard Area, lenders will require flood insurance. The cost of this policy depends on many factors, including:

The elevation of your finished floor relative to the BFE

The type of construction you choose

Whether a LOMA or LOMR-F is in place

To avoid delays in permitting or surprises in lending, it’s best to gather this information before you draw full plans.

Why Flood Planning Belongs in Phase 1

Flood zone issues aren’t just a construction detail—they’re a planning priority. If your property sits in a flood zone or has unusual elevation conditions, those factors affect everything from your foundation strategy to your construction timeline.

That’s why flood-related questions are included in our Feasibility Review Checklist. We ask these questions up front—before plans are drawn or bids are requested.

Whether your site requires a raised slab, engineered fill, or full elevation certificate, our team uses your answers to prepare a Conceptual Estimate that reflects the true scope. You’ll understand your risks and requirements—before committing to final plans.

Use our Feasibility Review Checklist to evaluate flood and drainage concerns early.

Download the Checklist →

Building in a Flood Zone? We Can Help You Plan It Right.

Don’t guess your way into a costly mistake. At Carroll Construction, we help clients identify flood risk and elevation needs early—before committing to construction plans. It’s part of our process. Use our tools, get expert guidance, and move forward with clarity.